Planning Beyond My Lifetime: A Mother’s RDSP Journey for Her Son’s Future

By: Ma Joannalyn Diaz

When our son Philip was diagnosed with Autism Spectrum Disorder (ASD) and ADHD at three years old, my world shifted quietly but permanently. I still remember sitting in that room, hearing the words, and feeling the ground move beneath me. It wasn’t loud or dramatic — it was slow, heavy, and deeply painful.

Like many mothers, my first instinct was to fight for him.

I researched endlessly. I watched videos late at night. I talked to specialists, therapists, teachers — anyone who could help me understand what Philip needed.

And like many parents, I went through denial.

I wanted to believe that autism was something he could “grow out of,” or something therapy could “fix.” I held on to the hope that maybe Philip was one of those children you see in movies — different, yes, but also gifted, brilliant, a genius waiting to be awakened.

But real life isn’t a movie. And slowly, reality settled in.

As Philip grew older, we began to understand his unique rhythm — his strengths, his challenges, his beautiful way of seeing the world. And with that understanding came acceptance: his life might not follow the path we once imagined.

That’s when the fear began.

Not the kind that comes and goes — but the kind that settles quietly in your heart. The fear of the future. The fear of the unknown. The fear of what happens when I’m no longer here to guide him.

There were nights I cried silently, thinking, If I could just live one day longer than my son, I could leave this world in peace. But life doesn’t work that way. And with every passing day, that fear settled deeper.

Eventually, I realized something important: Fear doesn’t help Philip. Planning does.

If I want to give him the closest chance to independence — or at least a life where he is supported, secure, and cared for — I need to build that future now, while I’m still here, while I’m still strong.

That’s how we discovered the Registered Disability Savings Plan (RDSP).

Photo taken by my husband, Felix Diaz — a moment with me, our son Philip, and our daughter Farrah.

What Every Parent Should Know About RDSP

From a mother who had to learn all of this the hard way.

When I finally learned about the RDSP, I realized it wasn’t just a financial plan — it was a way to love Philip into the future. Below is everything I wish I knew from the beginning.

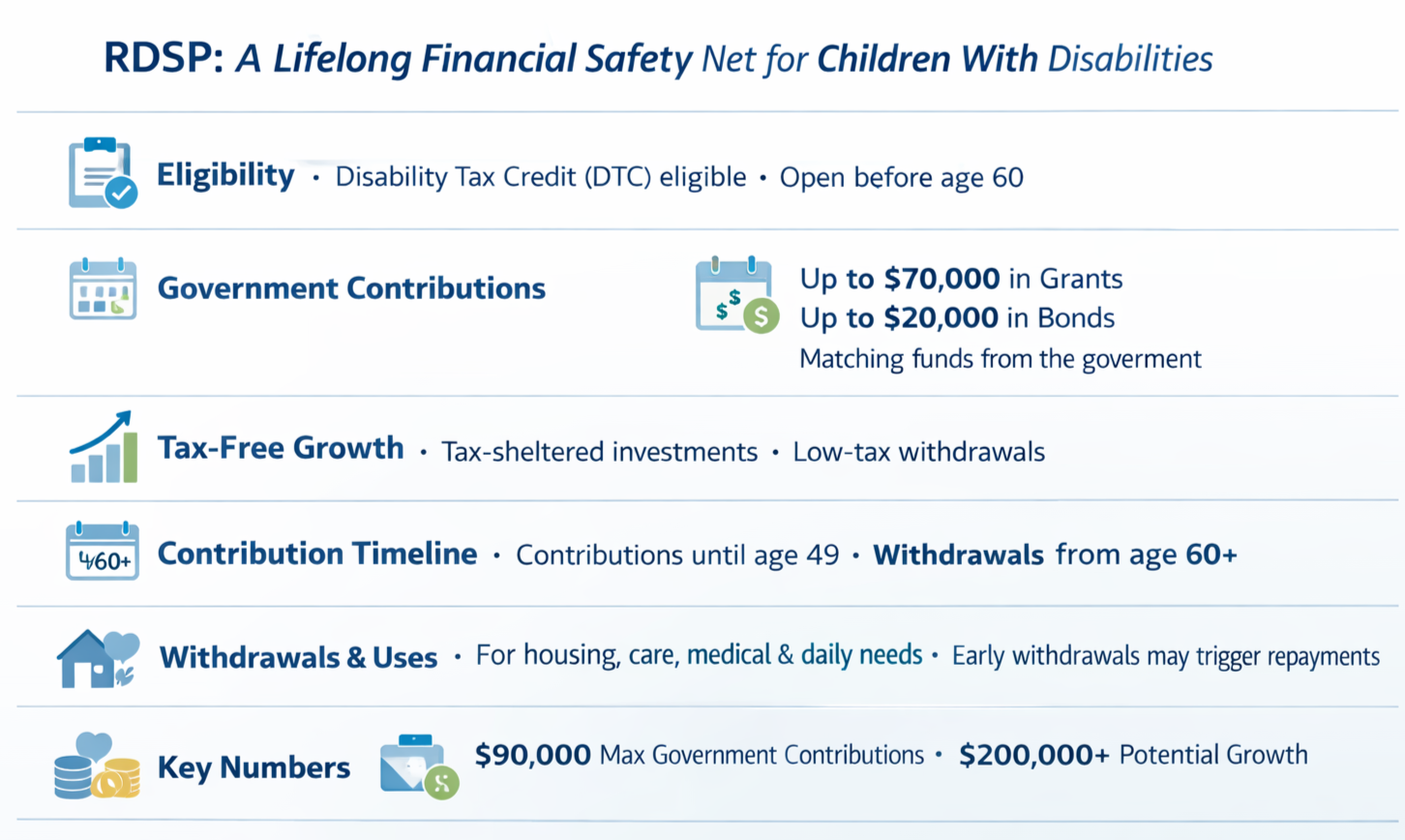

Eligibility — Who Can Have an RDSP?

Must qualify for the Disability Tax Credit (DTC)

Can open anytime before age 60

Must have a SIN and be a Canadian resident

Parent/guardian can open for minors or dependent adults

Adults can open their own RDSP if capable; otherwise a legal representative can

Government Contributions — The Part Most Parents Don’t Realize Is HUGE

Canada Disability Savings Grant (CDSG)

Up to $3,500/year

Up to $70,000 lifetime

Matching rates: 100%–300% depending on family income

Example: Contribute $1,000, government may add $3,000

Canada Disability Savings Bond (CDSB)

Up to $1,000/year

Up to $20,000 lifetime

No personal contributions required

Catch-Up Rules

You can receive up to 10 years of past grants and bonds if your child was eligible for DTC in previous years.

Tax-Free Growth — Why RDSP Works Best Over Decades

Investments grow tax-sheltered

Withdrawals later in life are usually taxed at very low rates

Ideal for long-term compounding

The earlier you start, the more powerful it becomes

Contribution Timeline — The RDSP Has a “Sweet Spot” Window

Government contributions stop at age 49

RDSP can stay open until age 60+

Best used as a decades-long growth plan

Lifetime contribution limit: $200,000

Withdrawals — When and How Your Child Can Use the Money

Two Types of Withdrawals

A. PDAP — Periodic Disability Assistance Payments

One-time withdrawals.

Can be taken anytime

Flexible

Useful for emergencies or major expenses

May trigger repayment (see 10-year rule)

B. LDAP — Lifetime Disability Assistance Payments

Regular, ongoing payments for life.

Must begin by the end of the year your child turns 60

Can start earlier

Designed as lifelong support income

The 10-Year Rule — The Most Important Thing to Understand

If you withdraw money within 10 years of receiving grants or bonds, you may need to repay some of the government contributions.

This means:

RDSP works best when left untouched for at least 10 years

The longer you wait, the more government money your child keeps

Ideally, withdrawals happen after age 30–40, when most grants/bonds have matured

What RDSP Funds Can Be Used For

There are no restrictions on how RDSP money is used. It can support:

Housing

Daily living

Medical needs

Therapies

Long-term care

Assistive devices

Support workers

Transportation

Education or training

Quality-of-life needs

Independence planning

RDSP is meant to support your child’s life — whatever that looks like.

Additional RDSP Benefits Most Parents Don’t Know

RESP to RDSP transfer: Up to $50,000 if your child won’t pursue post-secondary education

Does NOT affect disability benefits like AISH, ODSP, or provincial supports

Protected from creditors in most provinces

Flexible investment options: mutual funds, ETFs, GICs, bonds, conservative or growth portfolios

No annual contribution limit (only lifetime limit)

Infographic: A visual summary of the Registered Disability Savings Plan (RDSP), showing eligibility requirements, government grants and bonds, tax‑free growth, contribution timelines, withdrawal rules, and the long‑term financial benefits for children with disabilities.

A Mother’s Realization

It took time for me to accept Philip’s diagnosis — and even longer to accept that his future might require lifelong support. But once I did, something shifted inside me.

I stopped focusing on “fixing” him. I started focusing on supporting him. I stopped dreaming of a movie-like transformation. I started building a real-life plan.

RDSP became part of that plan.

It doesn’t erase the fear — nothing truly does — but it gives me a path forward. A way to prepare. A way to protect him. A way to give him dignity, stability, and choices later in life.

And for mothers like me, that means everything.

Final Message to Fellow Parents

Our children may not follow the path we once imagined. But they follow a path that is uniquely theirs — full of beauty, challenge, and meaning.

We can’t control everything. We can’t predict everything. But we can prepare.

And sometimes, preparation is the most loving thing we can do.

If you haven’t looked into RDSP yet, start today. Not because you’re giving up hope — but because you’re building it.

For Philip. For your child. For all of us walking this journey together.

Our children deserve a future built with intention, love, and security — and RDSP is one of the tools that helps us create that future.

Invitation to Connect

If you’d like to learn more or simply talk to someone who understands this journey, you can connect with us through the form on our website. We’re here to help you navigate this with clarity and compassion.